Updated on November 24th, 2023

There are countless ways to value stocks. There are methods based on cash flow, earnings, dividend yield, revenue, and the subject of this article, book value. The concept of book value is quite simple. The company’s assets have to be valued at least quarterly on the balance sheet for investors to see, and based upon that value, investors can then compare the market value of the stock to the asset value on the balance sheet.

By doing this, an investor can see if a stock trades below its theoretical liquidation value, which is the net value of the company’s assets minus the net value of its liabilities. For instance, if a company has $2 billion in assets and $1 billion in total liabilities, its book value would be $1 billion. That would be the theoretical value of the company if it were to close down and liquidate its assets. If the stock had a market cap of $500 million, that would be 50% of the book value.

In doing this, investors can screen for stocks that are trading quite cheaply, as most stocks never trade below book value, and for those that do, they tend not to stay there for long.

Sectors that tend to see stocks below book value are financials, utilities, and certain consumer staples. It can happen in any sector, but these are the ones that are most prone to it.

In this article, we’ll take a look at 10 stocks that are trading below book value and that also pay strong dividends.

We have created a spreadsheet of stocks (and closely related REITs and MLPs, etc.) with dividend yields of 5% or more…

You can download your free full list of securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

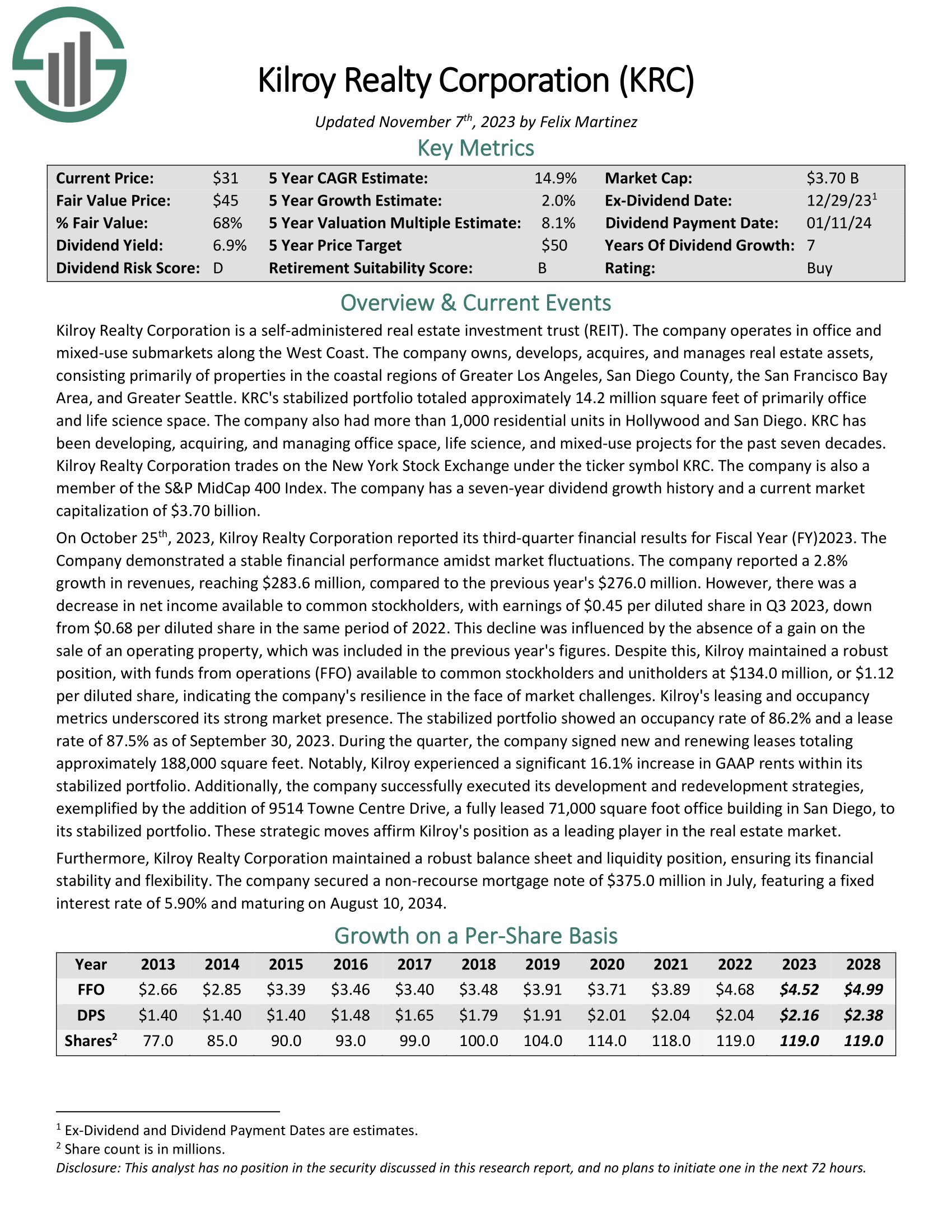

Kilroy Realty (KRC)

- Price-to-book ratio: 0.65

Kilroy Realty Corporation is a self-administered real estate investment trust (REIT). The company operates in office and mixed-use submarkets along the West Coast. The company owns, develops, acquires, and manages real estate assets, consisting primarily of properties in the coastal regions of Greater Los Angeles, San Diego County, the San Francisco Bay Area, and Greater Seattle.

KRC’s stabilized portfolio totaled approximately 14.2 million square feet of primarily office and life science space. The company also had more than 1,000 residential units in Hollywood and San Diego.

On October 25th, 2023, Kilroy Realty Corporation reported its third-quarter financial results for Fiscal Year (FY)2023. The company demonstrated a stable financial performance amidst market fluctuations. The company reported a 2.8% growth in revenues, reaching $283.6 million, compared to the previous year’s $276.0 million.

Kilroy maintained robust position, with funds from operations (FFO) available to common stockholders and unitholders at $134.0 million, or $1.12 per diluted share, indicating the company’s resilience in the face of market challenges. Kilroy’s leasing and occupancy metrics underscored its strong market presence. The stabilized portfolio showed an occupancy rate of 86.2% and a lease rate of 87.5% as of September 30, 2023.

Click here to download our most recent Sure Analysis report on KRC (preview of page 1 of 3 shown below):

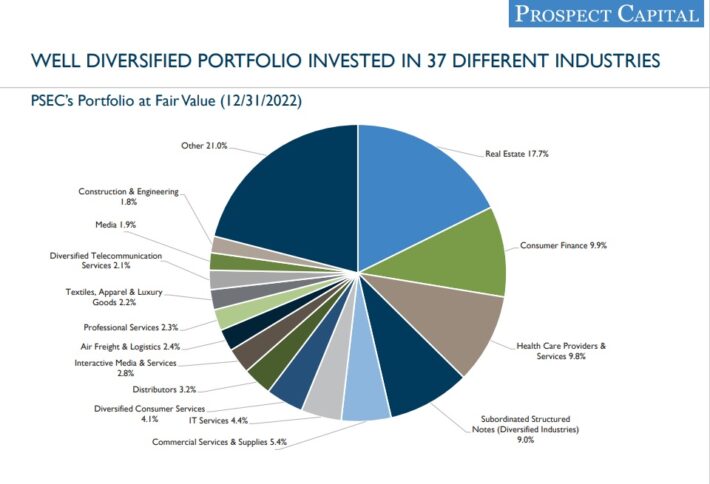

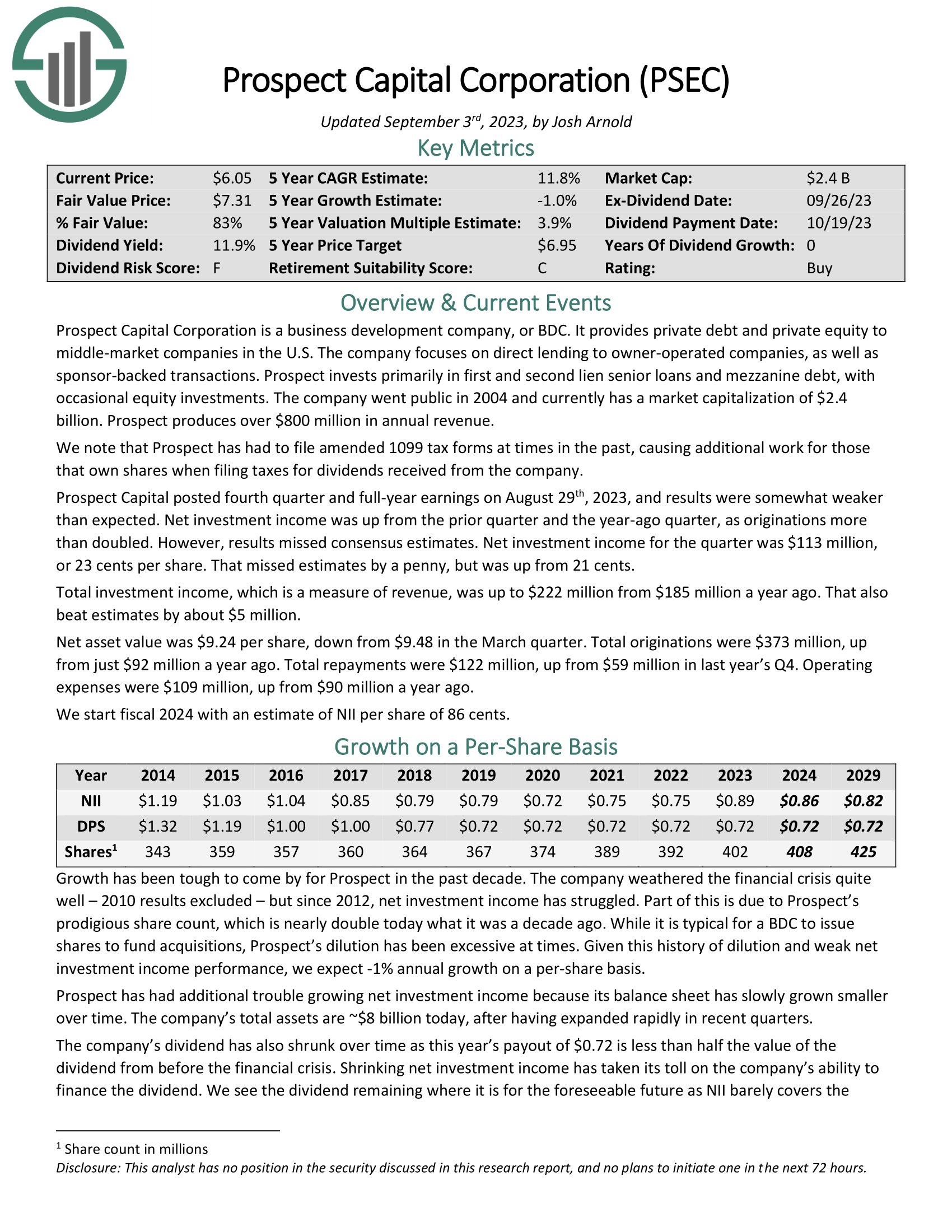

Prospect Capital (PSEC)

- Price-to-book ratio: 0.63

Prospect Capital Corporation is a Business Development Company, or BDC, that provides private debt and private equity to middle–market companies in the U.S. The company focuses on direct lending to owner–operated companies, as well as sponsor–backed transactions.

Prospect invests primarily in first and second lien senior loans and mezzanine debt, with occasional equity investments.

Source: Investor Presentation

Prospect Capital posted fourth quarter and full-year earnings on August 29th, 2023, and results were somewhat weaker than expected. Net investment income was up from the prior quarter and the year-ago quarter, as originations more than doubled. However, results missed consensus estimates. Net investment income for the quarter was $113 million, or 23 cents per share. That missed estimates by a penny, but was up from 21 cents.

Click here to download our most recent Sure Analysis report on PSEC (preview of page 1 of 3 shown below):

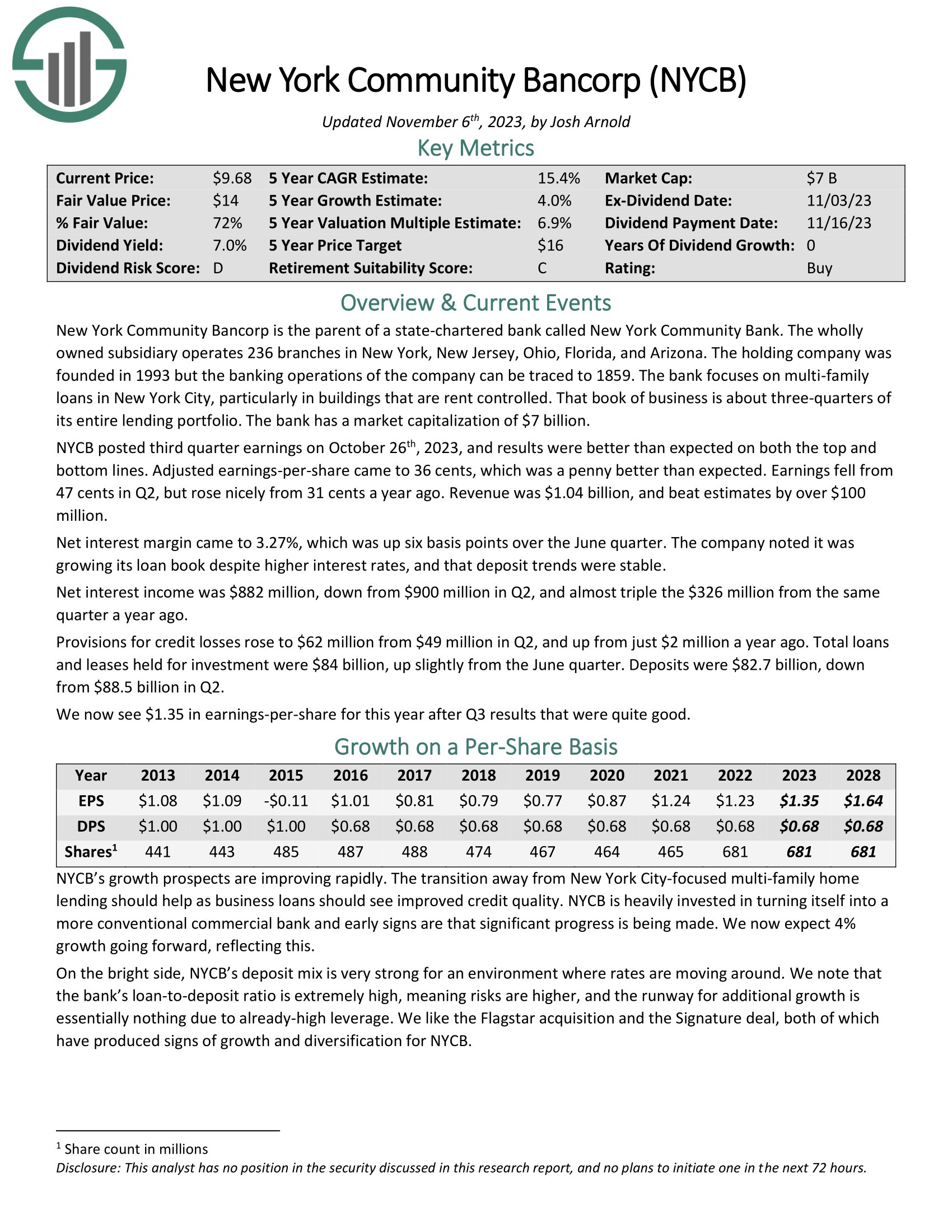

New York Community Bancorp (NYCB)

- Price-to-book ratio: 0.63

New York Community Bancorp is the parent of a state-chartered bank called New York Community Bank. The wholly owned subsidiary operates 236 branches in New York, New Jersey, Ohio, Florida, and Arizona. The holding company was founded in 1993 but the banking operations of the company can be traced to 1859.

The bank focuses on multi-family loans in New York City, particularly in buildings that are rent controlled. That book of business is about three-quarters of its entire lending portfolio.

NYCB posted third quarter earnings on October 26th, 2023, and results were better than expected on both the top and bottom lines. Adjusted earnings-per-share came to 36 cents, which was a penny better than expected. Earnings fell from 47 cents in Q2, but rose nicely from 31 cents a year ago. Revenue was $1.04 billion, and beat estimates by over $100 million.

Click here to download our most recent Sure Analysis report on NYCB (preview of page 1 of 3 shown below):

NextEra Energy Partners (NEP)

- Price-to-book ratio: 0.63

NextEra Energy Partners was formed in 2014 as Delaware Limited Partnership by NextEra Energy to own, operate, and acquire contracted clean energy projects with stable, long-term cash flows. The company’s strategy is to capitalize on the energy industry’s favorable trends in North America of clean energy projects replacing uneconomic projects.

NextEra Energy Partners operates 34 contracted renewable generation assets consisting of wind and solar projects in 12 states across the United States. The company also operates contracted natural gas pipelines in Texas which accounts for about a fifth of NextEra Energy Partners’ income.

On October 24, 2023, NextEra Energy Partners released its earnings report for the third quarter of 2023. The company reported quarterly earnings of $0.57 per share, surpassing the consensus estimate of $0.48 per share, but falling short of the $0.93 per share reported a year ago.

Click here to download our most recent Sure Analysis report on NEP (preview of page 1 of 3 shown below):

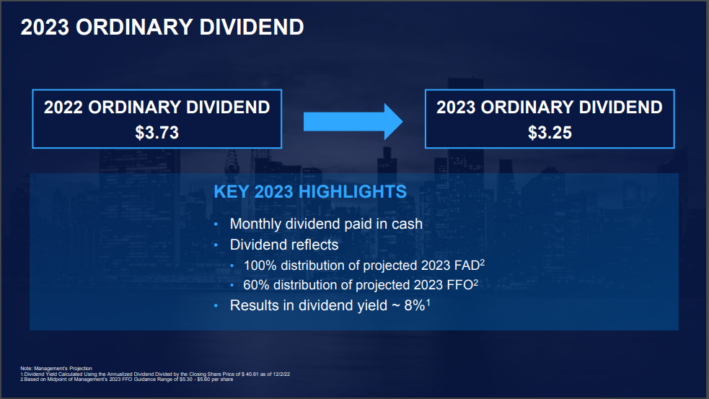

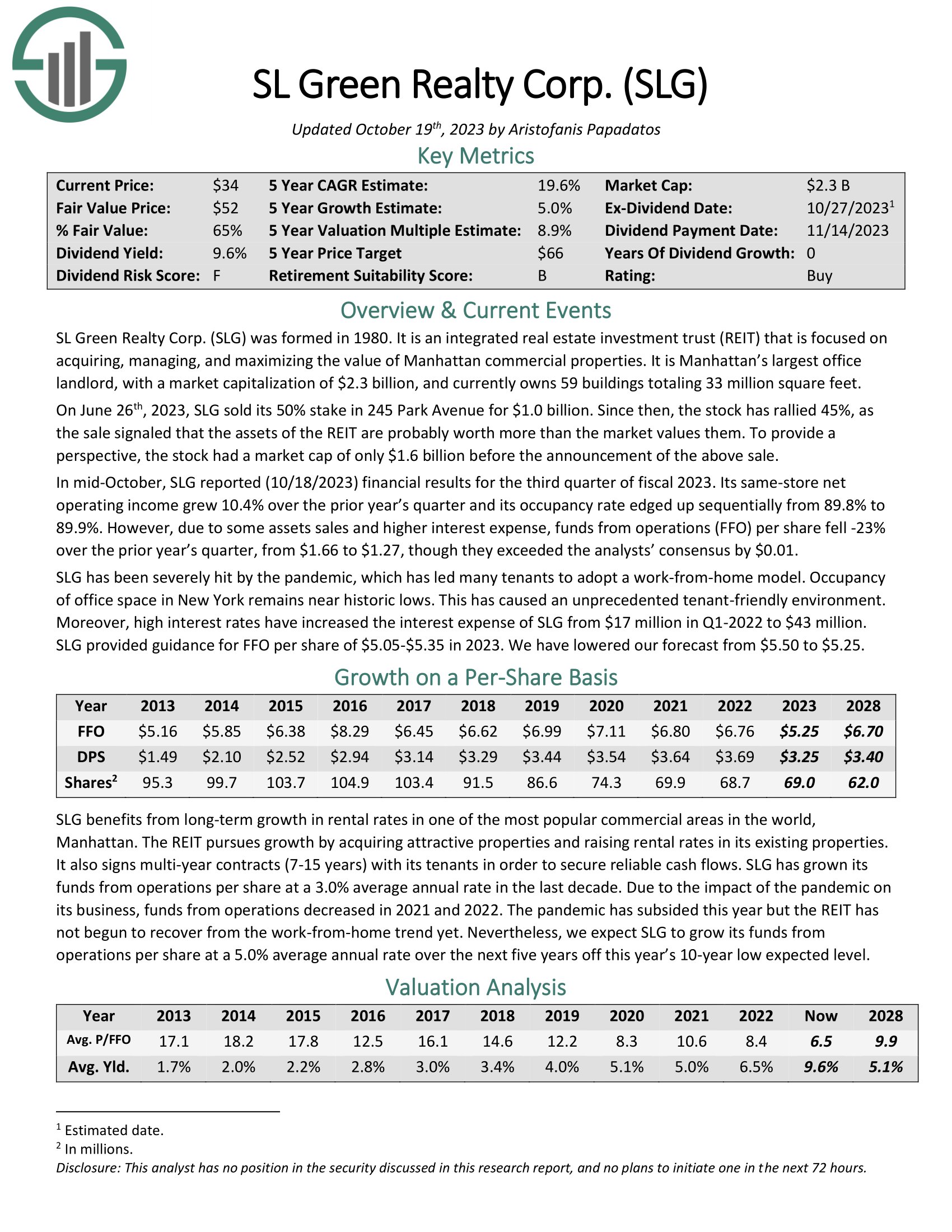

SL Green Realty (SLG)

- Price-to-book ratio: 0.61

SL Green is a self-managed REIT that manages, acquires, develops, and leases New York City Metropolitan office properties. In fact, the trust is the largest owner of office real estate in New York City, with the majority of its properties located in midtown Manhattan. It is Manhattan’s largest office landlord, with 60 buildings totaling about 33 million square feet.

Source: Investor Presentation

In mid-October, SLG reported (10/18/2023) financial results for the third quarter of fiscal 2023. Its same-store net operating income grew 10.4% over the prior year’s quarter and its occupancy rate edged up sequentially from 89.8% to 89.9%. However, due to some assets sales and higher interest expense, funds from operations (FFO) per share fell -23% over the prior year’s quarter, from $1.66 to $1.27, though they exceeded the analysts’ consensus by $0.01.

Click here to download our most recent Sure Analysis report on SL Green Realty Corp. (SLG) (preview of page 1 of 3 shown below):

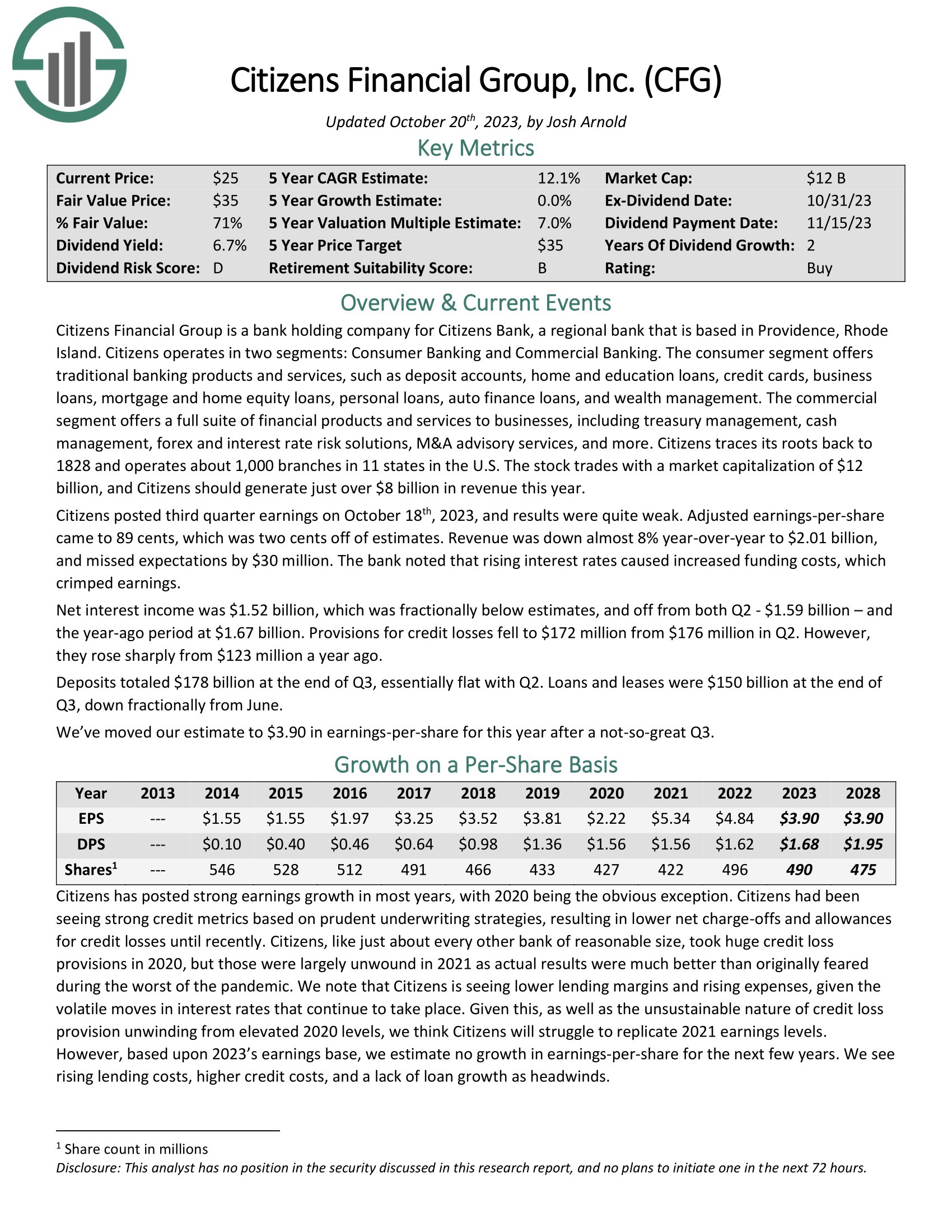

Citizens Financial Group (CFG)

- Price-to-book ratio: 0.60

Citizens Financial Group is a bank holding company for Citizens Bank, a regional bank that is based in Providence, Rhode Island. Citizens operates in two segments: Consumer Banking and Commercial Banking. The consumer segment offers traditional banking products and services, such as deposit accounts, home and education loans, credit cards, business loans, mortgage and home equity loans, personal loans, auto finance loans, and wealth management.

The commercial segment offers a full suite of financial products and services to businesses, including treasury management, cash management, forex and interest rate risk solutions, M&A advisory services, and more. Citizens traces its roots back to 1828 and operates about 1,000 branches in 11 states in the U.S.

Citizens posted third quarter earnings on October 18th, 2023, and results were quite weak. Adjusted earnings-per share

came to 89 cents, which was two cents off of estimates. Revenue was down almost 8% year-over-year to $2.01 billion, and missed expectations by $30 million. The bank noted that rising interest rates caused increased funding costs, which crimped earnings.

Click here to download our most recent Sure Analysis report on CFG (preview of page 1 of 3 shown below):

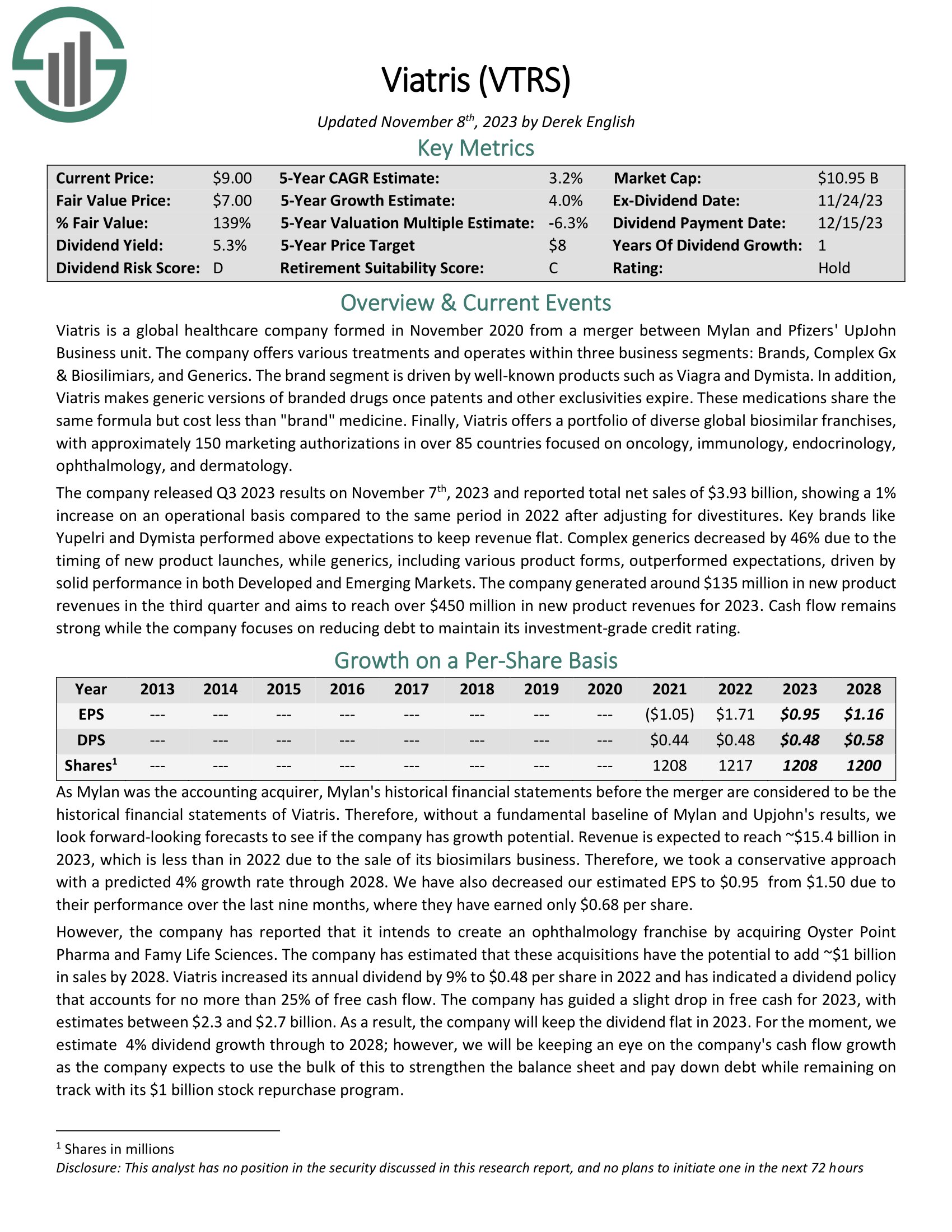

Viatris (VTRS)

- Price-to-book ratio: 0.55

Viatris is a global healthcare company formed in November 2020 from a merger between Mylan and Pfizers’ UpJohn Business unit. The company offers various treatments and operates within three business segments: Brands, Complex Gx & Biosilimiars, and Generics.

The brand segment is driven by well-known products such as Viagra and Dymista. In addition, Viatris makes generic versions of branded drugs once patents and other exclusivities expire. These medications share the same formula but cost less than “brand” medicine.

Finally, Viatris offers a portfolio of diverse global biosimilar franchises, with approximately 150 marketing authorizations in over 85 countries focused on oncology, immunology, endocrinology, ophthalmology, and dermatology.

The company released Q3 2023 results on November 7th, 2023 and reported total net sales of $3.93 billion, showing a 1% increase on an operational basis compared to the same period in 2022 after adjusting for divestitures. Key brands like Yupelri and Dymista performed above expectations to keep revenue flat.

Click here to download our most recent Sure Analysis report on VTRS (preview of page 1 of 3 shown below):

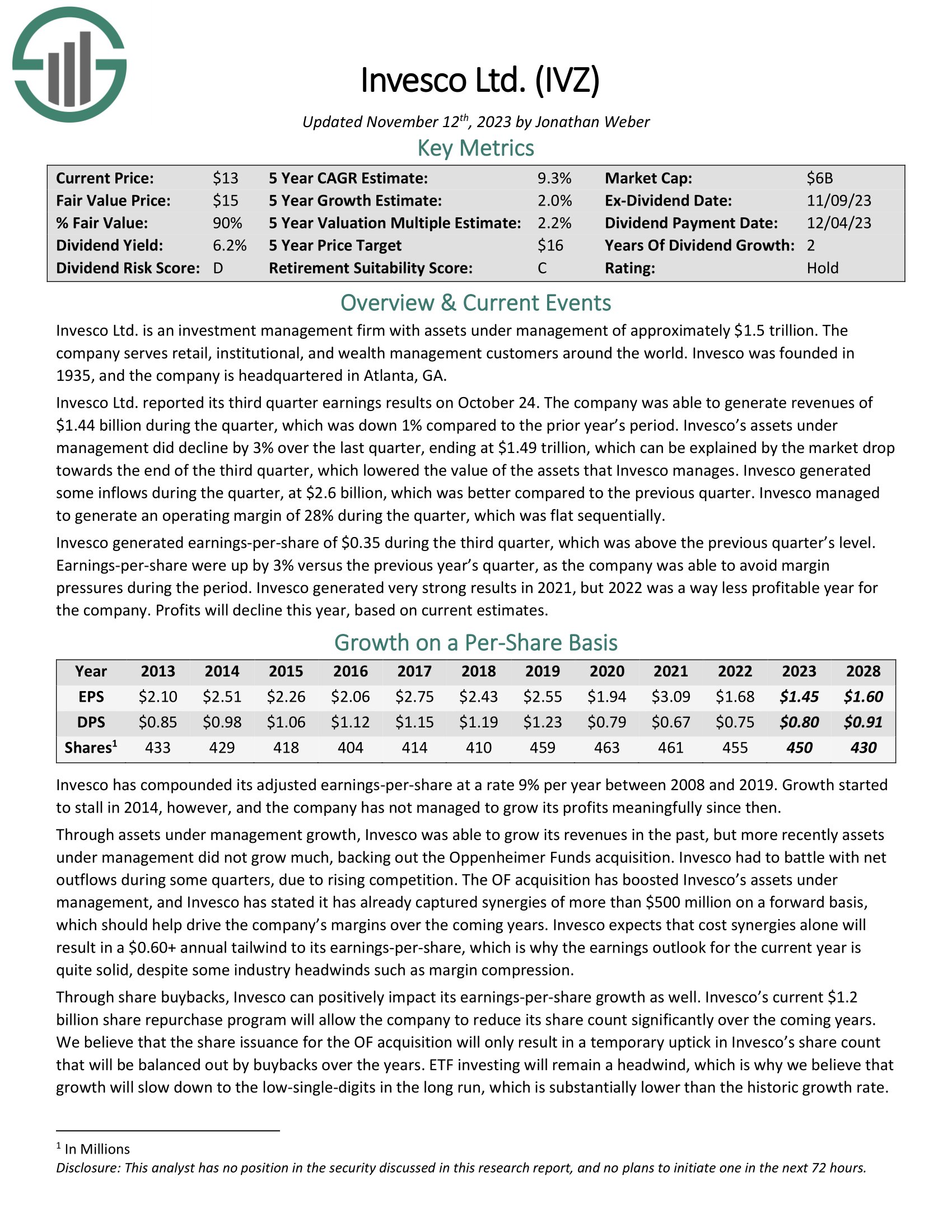

Invesco Ltd. (IVZ)

- Price-to-book ratio: 0.55

Our next stock is Invesco, a publicly-owned investment manager. The company provides investment products and services to institutions, individuals, funds, and pension funds. Invesco offers a wide variety of stocks, bonds, and related funds for customers to choose from.

Invesco Ltd. reported its third quarter earnings results on October 24. The company was able to generate revenues of $1.44 billion during the quarter, which was down 1% compared to the prior year’s period. Invesco’s assets under management did decline by 3% over the last quarter, ending at $1.49 trillion, which can be explained by the market drop towards the end of the third quarter, which lowered the value of the assets that Invesco manages.

Invesco generated inflows during the quarter, at $2.6 billion, which was better compared to the previous quarter. Invesco managed to generate an operating margin of 28% during the quarter, which was flat sequentially.

Invesco generated earnings-per-share of $0.35 during the third quarter, which was above the previous quarter’s level. Earnings-per-share were up by 3% versus the previous year’s quarter, as the company was able to avoid margin

pressures during the period.

Click here to download our most recent Sure Analysis report on Invesco Ltd. (preview of page 1 of 3 shown below):

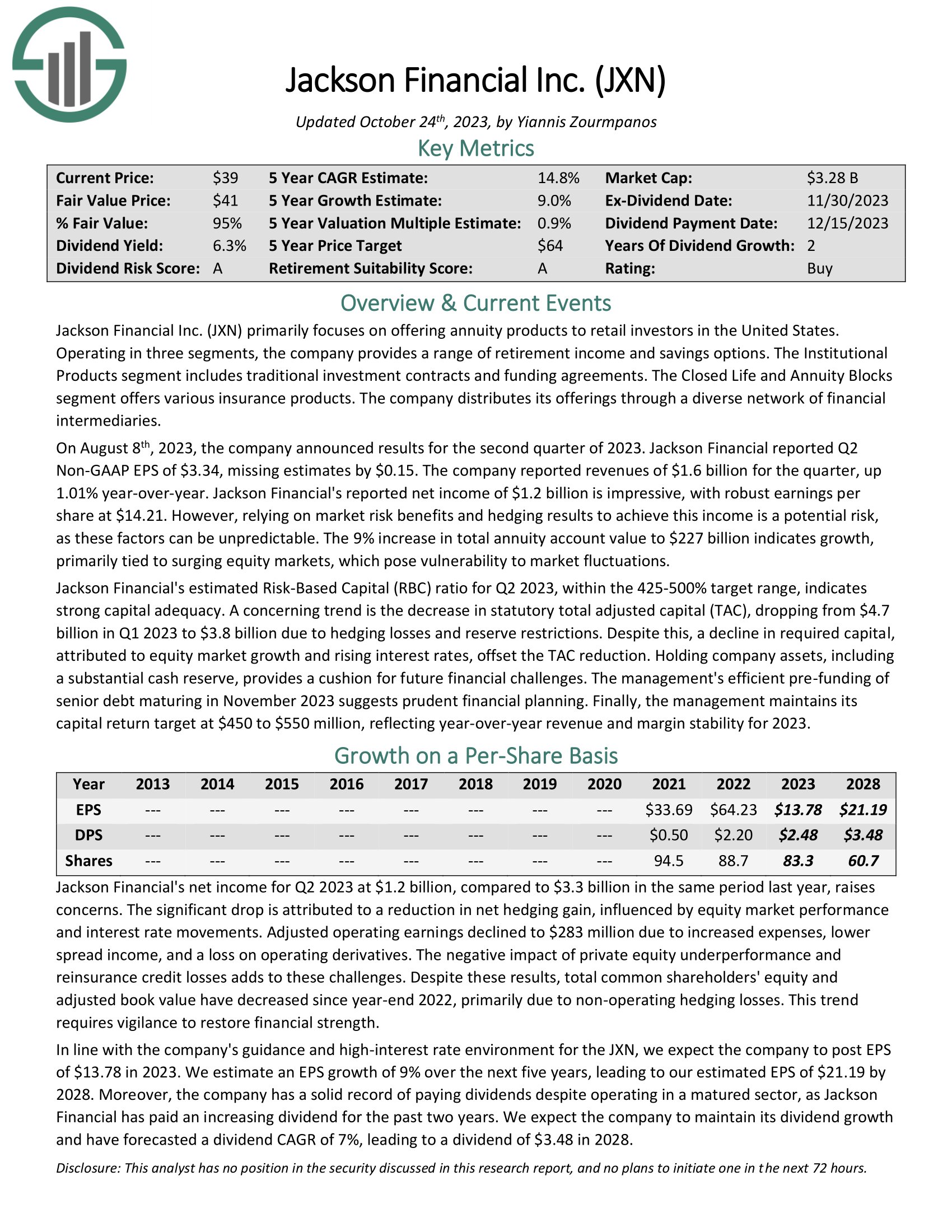

Jackson Financial (JXN)

- Price-to-book ratio: 0.42

Jackson Financial Inc. primarily focuses on offering annuity products to retail investors in the United States. Operating in three segments, the company provides a range of retirement income and savings options. The Institutional Products segment includes traditional investment contracts and funding agreements. The Closed Life and Annuity Blocks segment offers various insurance products. The company distributes its offerings through a diverse network of financial intermediaries.

On August 8th, 2023, the company announced results for the second quarter of 2023. Jackson Financial reported Q2 Non-GAAP EPS of $3.34, missing estimates by $0.15. The company reported revenues of $1.6 billion for the quarter, up 1.01% year-over-year. Jackson Financial’s reported net income of $1.2 billion is impressive, with robust earnings per share at $14.21. The 9% increase in total annuity account value to $227 billion indicates growth, primarily tied to surging equity markets, which pose vulnerability to market fluctuations.

Click here to download our most recent Sure Analysis report on JXN (preview of page 1 of 3 shown below):

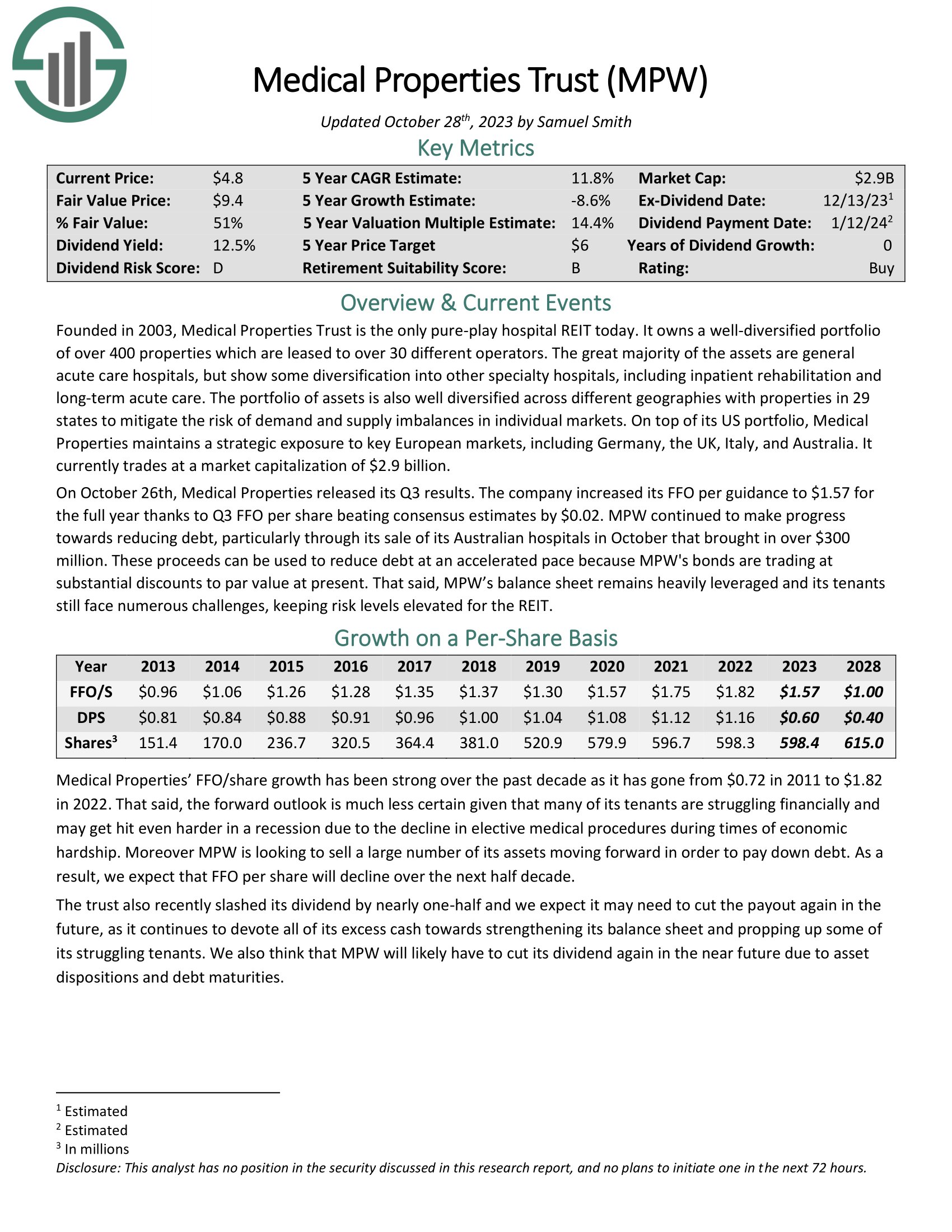

Medical Properties Trust (MPW)

- Price-to-book ratio: 0.34

Medical Properties Trust is the only pure-play hospital REIT today. It owns a well-diversified portfolio of over 400 properties which are leased to over 30 different operators. The great majority of the assets are general acute care hospitals, but show some diversification into other specialty hospitals, including inpatient rehabilitation and long-term acute care.

The portfolio of assets is also well diversified across different geographies with properties in 29 states to mitigate the risk of demand and supply imbalances in individual markets. On top of its US portfolio, Medical Properties maintains a strategic exposure to key European markets, including Germany, the UK, Italy, and Australia.

On October 26th, Medical Properties released its Q3 results. The company increased its FFO per guidance to $1.57 for the full year thanks to Q3 FFO per share beating consensus estimates by $0.02. MPW continued to make progress towards reducing debt, particularly through its sale of its Australian hospitals in October that brought in over $300 million.

These proceeds can be used to reduce debt at an accelerated pace because MPW’s bonds are trading at substantial discounts to par value at present. That said, MPW’s balance sheet remains heavily leveraged and its tenants still face numerous challenges, keeping risk levels elevated for the REIT.

Click here to download our most recent Sure Analysis report on MPW (preview of page 1 of 3 shown below):

Final Thoughts

While there is a wide variety of ways to value stocks, one way we like is to consider the company’s market value against its book value. This helps guard against overpaying for expensive stocks, and above, we noted ten stocks we like under book value today that also pay strong dividends.

Each has its unique combination of value, dividend yield, and growth; most are buy-rated based on total return potential.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.