Updated on October 13th, 2023

PepsiCo (PEP) recently increased its dividend by 10%. This marks the company’s 51st consecutive year of increased dividends paid to shareholders.

As a result, it is on the list of Dividend Kings.

The Dividend Kings are a group of just 50 stocks that have increased their dividends for at least 50 years in a row. We believe the Dividend Kings are among the highest-quality dividend growth stocks to buy and hold for the long term.

With this in mind, we created a full list of all 50 Dividend Kings. You can download the full list, along with important financial metrics such as dividend yields and price-to-earnings ratios, by clicking on the link below:

PepsiCo is a recession-proof Dividend King with a leadership position in the food and beverage industry. It is a reliable dividend growth stock that can increase its dividend, even during recessions.

At the same time, the stock has a market-beating 3.2% dividend yield. Due to its above-average yield and long history of consistent annual dividend increases, PepsiCo remains a high-quality holding for income investors.

Business Overview

PepsiCo is a major consumer staples stock. It has a large portfolio of quality brands, including more than 20 individual brands that generate annual sales of $1 billion or more. Just a few of its core brands include Pepsi, Frito-Lay, Quaker, Gatorade, and many more.

Source: Investor Presentation

Its business is nearly equally split between its food and beverage segments. It is also balanced geographically between the U.S. and the rest of the world.

On October 10th, 2023, PepsiCo announced third quarter results. Revenue increased 6.7% to $23.45 billion while adjusted earnings-per-share of $2.25 increased 14% year-over-year. Organic sales increased 8.8% for the third quarter. For the quarter, beverage volume was flat while convenient foods were down 2%.

PepsiCo Beverages North America’s revenue grew 9% organically as higher prices more than offset a 4.5% decline in volume. Frito-Lay North America increased 12%, again due to price increases, while volume was flat. Quaker Foods North America grew organic sales 6% despite a 3% decline in volume.

PepsiCo provided an updated outlook for 2023 as well, with the company expecting adjusted earnings-per-share of $7.54 for the year, up from $7.47, $7.27, and $6.93 previously. Organic sales are still projected to be higher by 10% for the year.

Growth Prospects

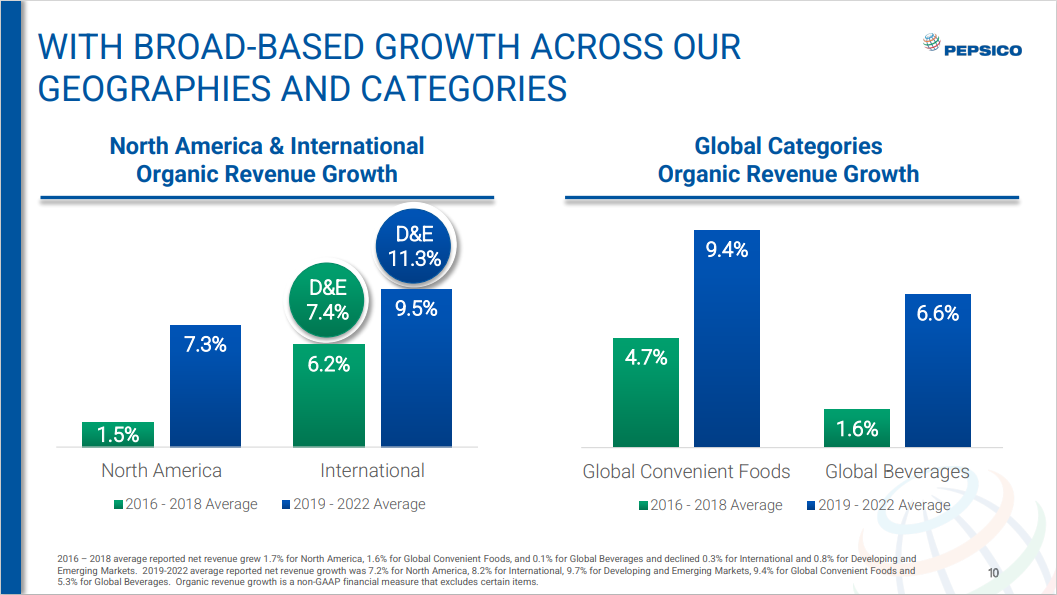

PepsiCo has a long history of steady growth. Even in a challenging environment for soda, PepsiCo has continued its consistent growth. An illustration of the company’s performance over the past several years can be seen in the below image.

Source: Investor Presentation

We believe PepsiCo will generate around 5%-6% adjusted earnings-per-share growth per year over the next five years. Going forward, two of PepsiCo’s most promising catalysts are growth in healthier foods and beverages, and in emerging markets.

Sales of soda are slowing down in developed markets like the U.S., where soda consumption has steadily declined for over a decade.

As a result, large soda companies like PepsiCo have had to adapt to a more health-conscious consumer. To do this, PepsiCo has shifted its portfolio toward healthier foods that are resonating more strongly with changing consumer preferences.

In addition, PepsiCo has a huge growth opportunity in emerging markets like China, Africa, India, and Latin America. These are under-developed regions of the world with large consumer populations and high economic growth rates.

Emerging markets were a growth driver once again last quarter. Latin America revenue increased 12%, Asia Pacific/Australia/New Zealand/China region improved 7%, and Africa/Middle East/South Asia was up 20%. Each region saw an uptick in volume.

Competitive Advantages & Recession Performance

PepsiCo has numerous competitive advantages. Among them are strong brands and a global scale. In all, PepsiCo has over 20 individual brands that each collect at least $1 billion in annual revenue. Strong brands give PepsiCo optimal shelf space at retailers and give the company pricing power.

PepsiCo’s financial strength also allows the company to invest in research and development, as well as advertising, to retain its competitive advantages.

For example, PepsiCo invests billions each year in research and development to innovate new products and packaging designs. In addition, PepsiCo regularly spends more than $2 billion each year on advertising to maintain market share and build brand equity with consumers.

PepsiCo’s competitive advantages and strong brands make the company highly profitable, even during recessions. Food and beverages always retain a certain level of demand, which is why the company held up so well during the Great Recession.

Source: Investor Presentation

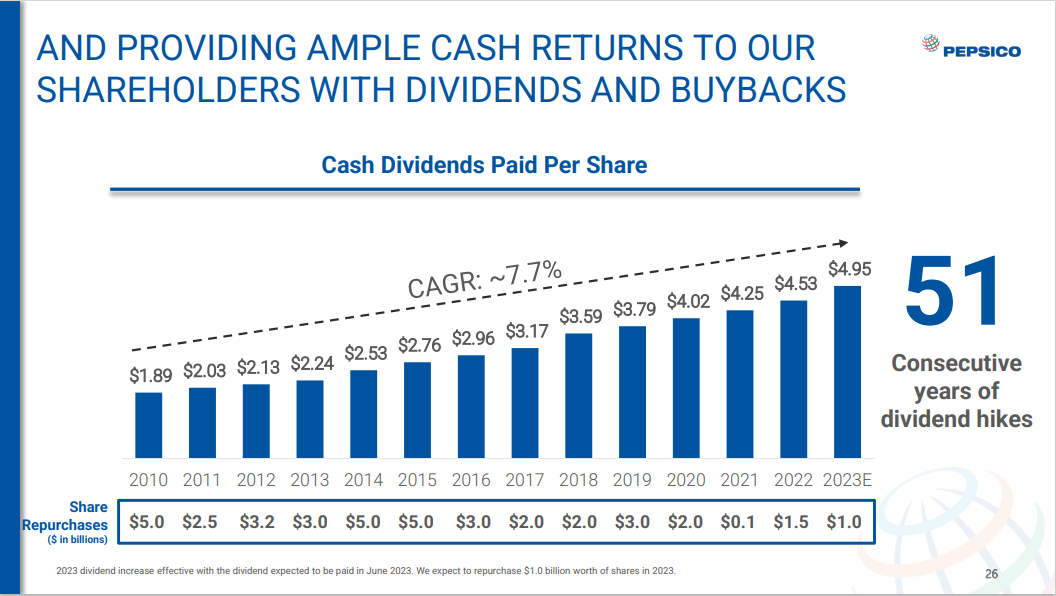

PepsiCo’s competitive advantages and profitability have enabled the company to increase its dividend for fifty years straight. Since 2010, PepsiCo has increased its dividend by 8% per year on average.

PepsiCo’s earnings-per-share throughout the Great Recession of 2007-2009 are listed below:

- 2007 earnings-per-share of $3.34

- 2008 earnings-per-share of $3.21 (3.9% decline)

- 2009 earnings-per-share of $3.77 (17% increase)

- 2010 earnings-per-share of $3.91 (3.7% increase)

As you can see, PepsiCo’s earnings-per-share declined only modestly in 2008. The company proceeded to grow earnings by nearly 20% in 2009, which is very impressive. Earnings continued to grow once the recession ended.

The company reported strong growth in 2020 and 2021 when the coronavirus pandemic sent the U.S. economy into a recession. Therefore, PepsiCo is a recession-resistant business.

Valuation & Expected Returns

PepsiCo is expected to generate earnings-per-share of $7.54 for 2023. Based on this, the stock trades for a price-to-earnings ratio of 21.2. Our fair value estimate is a price-to-earnings ratio of 21.0. As a result, the stock is just slightly overvalued. A declining price-to-earnings ratio could reduce annual returns by 0.2% each year over the next five years.

As a result, future returns will likely be comprised of earnings-per-share growth and dividends. We expect PepsiCo to grow earnings-per-share each year by 5.5%, consisting of organic revenue growth, acquisitions, and share repurchases.

In addition, PepsiCo also has a 3.2% current dividend yield. The combination of valuation changes, earnings growth, and dividends results in total expected returns of 8.5% per year over the next five years.

We currently rate PepsiCo stock a hold.

PepsiCo has a secure dividend, with a projected dividend payout ratio of 67% for 2023. This gives PepsiCo enough room to continue increasing the dividend at a rate in-line with the growth rate of its adjusted EPS.

Final Thoughts

PepsiCo is a high-quality company with a diverse portfolio of strong brands. Its long-term growth will be fueled by its snacks business and by advancing in developing markets.

The company has increased its dividend for 50 years in a row, and the stock currently yields 3.2%. Therefore, it meets our definition of a blue-chip stock, and it should continue to deliver steady dividend increases each year.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.